Review of the German M&A market in 2024 and outlook for 2025

1. Introduction

In 2024, the German M&A market was impacted by economic, political, and financial headwinds. The transaction environment was influenced by both geopolitical uncertainties — particularly due to elec-tions in the USA and Europe — and the persistent valuation gap between current market expectations and previous acquisition prices.

The following sections discuss the trends, developments, and challenges which have shaped the German M&A landscape in 2024. Assessments are made regarding the possible development of these trends in 2025. Additionally, the authors provide strategic recommendations for companies in this evolving market environment.

2. Reflecting on the year 2024

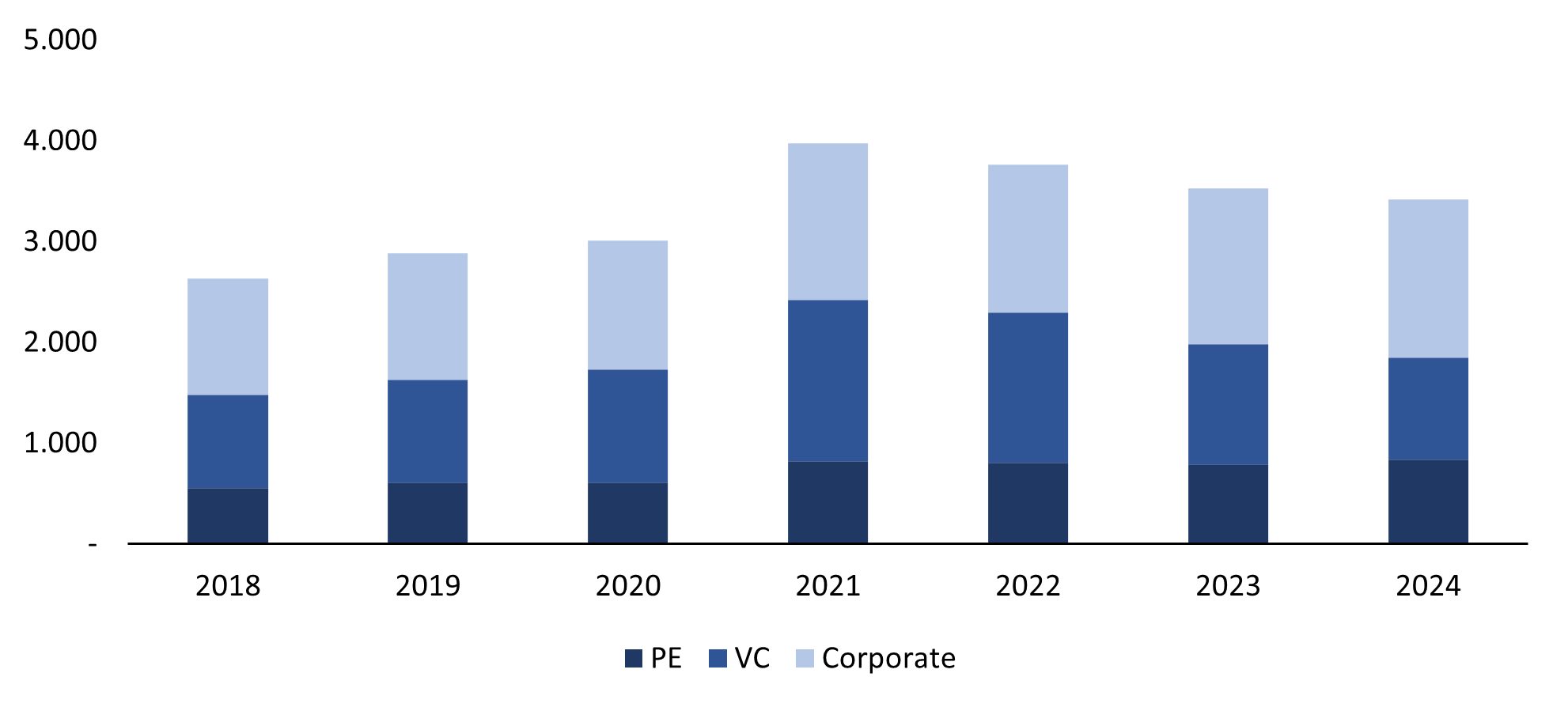

The number of announced M&A transactions decreased in 2024, totalling 3,418 (according to Pitch-Books), representing a 3% decrease from prior year. The number of Venture Capital (VC) transactions was particularly affected, with a decline of 14%. Overall, the M&A market is showing signs of recovery after a three-year downturn. The decline has slowed significantly, from 6% in 2023 to 3% in 2024.

Figure 1: Number of M&A Transactions in Germany, 2018 – 2024

Source: PitchBook (2024)

Source: PitchBook (2024)

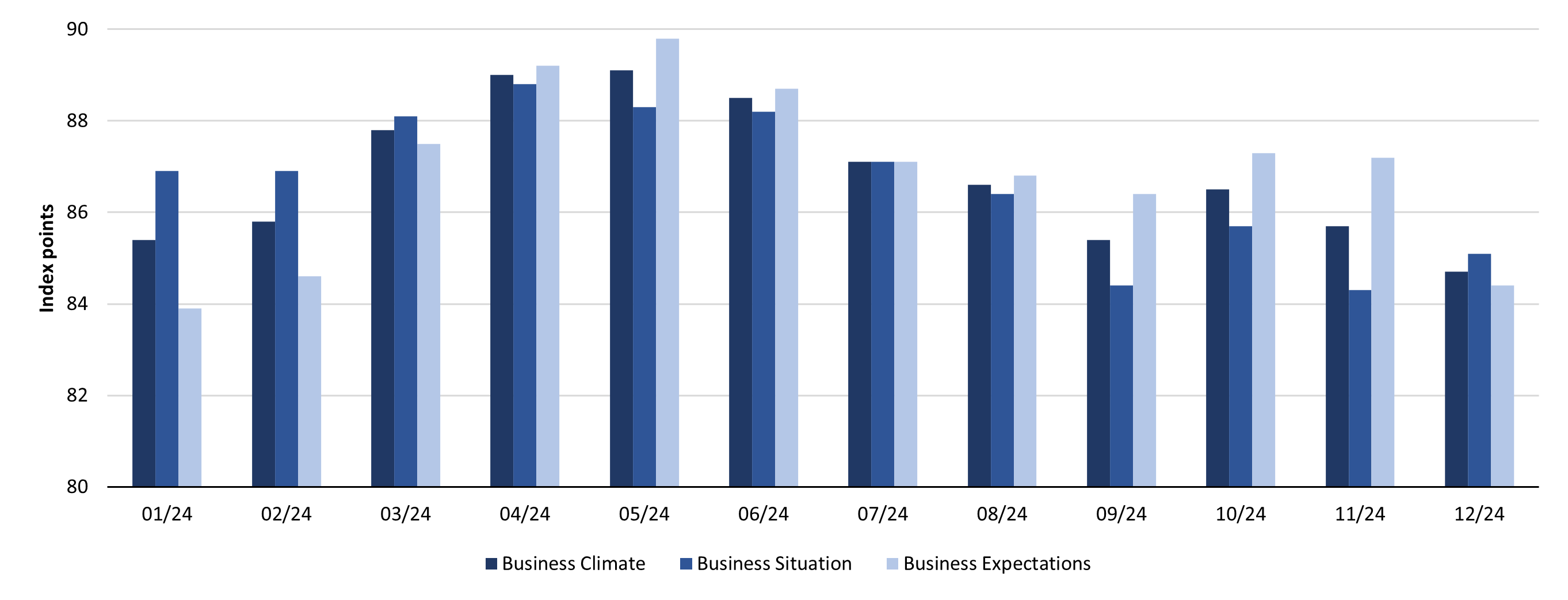

In 2024, the M&A environment benefited from a recovery in the business sector. However, uncertainties emerged during the second half of the year, predominantly driven by the results of the presidential elec-tions in the United States and the collapse of the German government.1 From an economic perspective, Germany continued to face significant challenges. The International Monetary Fund forecasts Germany's GDP to remain stagnant in 2024, following a 0.3% decrease in the previous year. This puts Germany behind the rest of the EU, which is anticipated to experience GDP growth of 1.1% in 2024, up from 0.6% in the previous year.2 Germany’s economic challenges are often attributed to the requirements of transitioning to a CO2-neutral economy and the effects of demographic change. Additionally, the export-driven nation faces challenges in the global market due to increasing protectionism.3

Figure 2: Business Climate, Business Situation, and Expectations for Germany based on the Ifo Institute for the Year 2024

Source: ifo Institut (2024)

Source: ifo Institut (2024)

Relief factors in the M&A market included easing inflation and, consequently, an improved financing envi-ronment. The Harmonized Consumer Price Index (HICP) for food decreased by approximately 3 index points on average in the first quarter of 2024, while the HICP for non-energy industrial goods decreased by approximately 1.4 index points. In contrast, prices for services remained resilient, showing only a slight decrease of 0.3 index points. Meanwhile, energy prices increased by an average of 4 index points com-pared to the previous quarter.4

Despite the European Central Bank’s (ECB) gradual reduction of the main refinancing rate from 4.5% in September 2023 to 3.15% in December 2024, corporate investments and new lending continued to de-cline. This is predominantly attributable to banks’ tightening of credit policy requirements due to the economic downturn, fears of recession, and a reduced risk appetite.5

The aforementioned macroeconomic and political factors have led to changes in the nature of transac-tions over the past few years:

1. In 2024, as in 2023, a new peak in insolvencies was recorded, leading to an increase in the number of ‘distressed’ corporate transactions. Consequently, the number of insolvency filings in November 2024 increased by 12.6% compared to the same month the previous year.6 Notable examples of insolvencies in 2024 include the fashion giant Esprit and Galeria Karstadt Kaufhof.

2. The growing number of companies facing crises or insolvency has also led to a greater use of Debt-to-Equity-Swaps, which involve converting creditors' claims into equity to support the continued operation of a business. In 2023 alone, 23 such swaps were undertaken, which is twice as high as the annual average of the previous five years.7 A new record high is expected in 2024.

3. Furthermore, the emergence of illiquid markets made state intervention necessary. In Sep-tember 2024, the German government and the state of Lower Saxony signed contracts to take over approximately 80% of the shipbuilding company Meyer Werft GmbH, which had been impacted by the COVID-19 pandemic and increasing energy and raw material prices. There are also ongoing discussions about state involvement in the Kiel-based shipbuilder Thyssenkrupp Marine Systems.

4. The following analysis presents the M&A transactions in Germany registered in public data-bases for 2024.8 Although larger transactions exceeding 500 million euros accounted for over 61% of the total registered transaction volume, there is an ongoing trend towards smaller acquisitions and mergers, as in prior year. More than half of the 756 transactions analysed had volumes rang-ing from 10 to 100 million euros. The following table provides an overview of the number and volume of transactions across different size categories.

The comparison with other countries in the region indicates that the M&A activity recovery has been generally slower elsewhere. In EMEA as a whole, approximately 3,660 transactions were announced in the third quarter of 2024, representing a 5.2% decrease compared to the third quarter of 2023, with many European countries facing political and economic hinderances to M&A activities. In France, for example, high social security contributions and stricter labour laws are seen as obstacles to M&A activity, while in Italy, energy costs play a significant role, particularly for industries importing gas. In contrast, countries with above-average GDP growth experienced positive M&A activity trends. For instance, the United Kingdom, where GDP is forecast to increase by 1.1%, experienced a 12% increase in M&A trans-actions in the third quarter compared to the same quarter in prior year.9

Fig. 3 Distribution of transactions by size (in million EUR)

Source: PitchBook (2024), Mergermarket (2024) and CapitalIQ. (2024). M&A Transactions in 2024 (by announcement date) in Germany [Dataset].

Source: PitchBook (2024), Mergermarket (2024) and CapitalIQ. (2024). M&A Transactions in 2024 (by announcement date) in Germany [Dataset].

3. Current Developments and Outlook for 2025

The German M&A market is anticipated to experience moderate growth in 2025, supported by improved financing conditions, economic growth, and opportunities in sectors such as biotechnology. After two years of contraction, an uplift in Germany’s GDP of 0.8% is forecast, remaining vulnerable to weak global export demand and competition from China.10,11 This trend is likely to slightly reduce financing costs, particularly for private equity (PE) firms heavily reliant on debt. Nevertheless, it is anticipated that, given stabilising inflation, PE firms, will focus on innovative strategies, such as continuation funds, to generate liquidity.

The development of the German M&A market is influenced by both existing growth drivers and new op-portunities. Capital markets are thriving, offering a solid foundation for investments through decreasing interest rates and a stabilising economic environment. Additionally, structural changes are forcing com-panies to adapt to new market conditions through strategic acquisitions to secure competitive ad-vantages. These adjustments are key for addressing long-term trends such as digitalisation and ESG factors.

The political landscape will also play a central role in M&A activities in 2025. While uncertainties related to the U.S. presidential elections resulted in a downward transaction trend in the second half of 2024, historical patterns suggest a potential rebound of cross-border transactions in the first quarter of 2025. The anticipated political decisions in the U.S. will influence global investor confidence and transaction strategies.1 Meanwhile, the German federal elections in February 2025 will have an impact on the busi-ness climate and investment activity. A business-friendly government will create a more predictable regulatory environment, strengthening transaction volumes in the second half of the year and favouring strategic acquisitions. Additionally, a potential shift in the debt brake policy could expand fiscal flexibility, facilitating new growth investments.The healthcare and biotechnology sectors will also see strong transaction volumes, as companies seek to drive innovation through acquisitions. Medtech companies and biotech firms with robust R&D pipelines, particularly in personalised medicine and medical devices, will continue to offer attractive investment opportunities.

Despite ongoing challenges in the German industrial sector, increased M&A activity is anticipated in the industrial and chemicals sectors. Industrial companies with strong balance sheets are likely to pursue strategic acquisitions to offset stagnating domestic demand and strengthen their market position through geographic diversification and cost synergies.1,12

Across Europe, sovereign wealth funds, particularly those from the Middle East, will continue to be active players in capital-intensive industries such as renewable energy and infrastructure projects. The energy transition remains a key driver, as investors target sustainable and climate-friendly projects to pursue long-term ESG goals.

However, the overall economic recovery in Germany continues to be reliant on political stability, business confidence, and external economic factors such as global trade developments and U.S. fiscal policy. While the outlook for 2025 suggests cautious optimism for German mergers and acquisitions, the pace of recovery will depend on companies’ and investors’ ability to adapt to evolving market conditions. The combination of stabilising inflation, supportive monetary policy, and sector-specific innovation provides a solid foundation for growth. However, the ongoing uncertainties highlight the importance of strategic adaptability in order to capitalise on the opportunities in this volatile environment.

4. Strategic Implications for Investors in the Current M&A Environment

Die vergangenen Jahre turbulenter finanzieller und politischer Rahmenbedingungen haben den M&A-Lebenszyklus verlängert und detailorientierter gestaltet, da Investoren zunehmend darauf bedacht sind, Risiken zu minimieren und ihre Zielunternehmen vor Abschluss der Transaktion gründlich zu prüfen. Dies erhöht den Druck auf Investoren, ihre Investmentthese mit präzisen Finanzdaten zu untermauern.

In light of this, the authors would like to present some recommendations for companies and investors going forward.

Analysis of One's Own M&A History, Strategic Focus, and Exit Readiness:

An analysis of past M&A activities is crucial for identifying patterns, refining strategies, and avoiding prior mistakes. Companies should assess whether prior transactions have achieved strategic objectives such as market expansion or product diversification. This evaluation requires a clear alignment of acquisitions with the company's long-term goals, ensuring each transaction’s contribution towards greater strategic ambitions.

Exit readiness

Exit-Readiness should be a top priority. Sellers must ensure that all transaction-relevant documents, such as financial reports and legal paperwork, are up-to-date, complete, and detailed. A proactive approach to exit prepa-ration streamlines transactions and enhances credibility with potential buyers. In an environment with extended timelines and increased scrutiny, well-structured documentation provides a competitive ad-vantage and helps minimise delays.

Due-Diligence-Processes:

The preparation and execution of the due diligence process are key success factors. Buyers must ensure that financial metrics, operational indicators, as well as legal and tax risks, are accurately represented. Given the evolving business landscape, financial evaluations must be complemented by analyses of ESG compliance, cybersecurity, and technological compatibility. ESG factors are increasingly influencing corpo-rate valuations and access to capital.

Post-Merger-Integration and Risk Management:

A successful post-merger integration (PMI) is crucial for the success of a transaction. In addition to finan-cial and operational synergies, cultural alignment is essential. Companies should learn from previous integrations to identify challenges early on and develop targeted strategies. A structured integration plan should foster collaboration, streamline processes, and retain key talent.

Retaining key employees after an acquisition is vital in a competitive labour market. Companies should implement measures such as incentive programmes, training, and a positive work environment. These initiatives minimise disruptions and unlock the full value of the transaction.

The acquired company should establish structured reporting that ensures proactive risk identification and mitigation. This includes using modern data analytics tools (e.g., interactive dashboards) and scenario planning tools (e.g., for liquidity forecasting) to predict potential risks and assess their impact. For exam-ple, stress testing financial models can help companies assess their resilience under unfavourable market conditions, while simulations of regulatory changes can provide insights into potential compliance vulner-abilities.

Real-time monitoring mechanisms for KPIs enable companies to respond quickly to unexpected develop-ments. By implementing these advanced practices, companies can identify hidden strategic and financial opportunities, ensuring long-term success.

5. Conclusion

The 2025 outlook for the German M&A market reflects a cautiously optimistic scenario, driven by stabi-lising inflation, favourable financing conditions, and sector-specific innovation. Moderate economic growth is expected to serve as a catalyst for a rebound in transaction volumes, particularly in the TMT, healthcare, and industrial sectors. The easing of political uncertainties in Germany and the United States will be instrumental in restoring business confidence and creating a more predictable investment envi-ronment. Companies and investors that prioritise strategic adaptability, technological integration, and thorough preparation will be best positioned to capitalise on M&A opportunities in this dynamic market.

1 Jens, P. (2024): Sorgen mittelständischer Firmen: „In diesem Umfeld investiert niemand“. Was Ampel-Aus und Trump-Wahl für den Mittelstand bedeuten | tagesschau.de; retrieved on 23. Dec. 2024

2 International Monetary Fund: World Economic Outlook Database (October 2024); retrieved on 23. Dec. 2024

3 Deutsche Bundesbank (2024): Deutschland-Prognose: Wachstumsaussichten deutlich eingetrübt | Deutsche Bundesbank; retrieved on 23. Dec. 2024

4 Eurostat (2024): Inflation rate of the European Union 2002 – 2024, by category; retrieved on 4. Dec. 2024

5 Schneider, T. (2024): Aktuelle Entwicklungen im Finanzierungsumfeld, in: M&A Review; retrieved on 23. Dec. 2024

6 Statistisches Bundesamt (2024): Gewerbemeldungen und Insolvenzen

– Statistisches Bundesamt; retrieved on 23. Dec. 2024

7 Schultze & Braun (2024): Debt-Equity-Swap: Komplex, aber mit großem Potential; retrieved on 27. Dec. 2024

8 Capital IQ, Mergermarket, PitchBook (2024). M&A Transactions in 2024 in Germany; As of: 30. Nov. 2024

9 Frazer, J. (2024): Deal Drivers: EMEA Q3 2024. A spotlight on mergers and acquisitions trends in 2024; retrieved on 16. Dec. 2024

10 European Central Bank (2024). Key ECB interest rates: www.ecb.europa.eu/stats/policy_and_exchange_rates/key_ecb_interest_rates/html/index.en.html; retrieved on 16. Dec. 2024

11 Reuters (2024). Big banks expect a quarter-point cut for ECB‘s first meeting of 2025: www.reuters.com/markets/europe/big-banks-expect-quarter-point-cut-ecbs-first-meeting-2025-2024-12-13/?utm_source=chatgpt.com; retrieved on 16. Dec. 2024

12 ION Analytics & CMS Law Tax Future (2024). Back in Gear: European M&A Outlook 2025: https://ionanalytics.com/insights/mergermarket/back-in-gear-european-ma-outlook-2025/; retrieved on 12. Dez. 2024