Review of the German M&A market in 2024 and outlook for 2025 – spotlight on the private equity M&A market

1. Introduction

M&A activities in Germany were subdued in 2024, with the market heavily influenced by global challenges such as geopolitical tensions, an uncertain interest rate environment, pivotal elections and the ongoing structural transformation of Germany’s industrial landscape. At present, these factors are making it difficult to pinpoint where the market is heading.

Germany’s M&A market nevertheless has a lot to offer, particularly for private equity firms. Although the country is renowned for its solid SME sector and the ubiquity of family-owned businesses, private equity firms have not yet made their mark on Germany's M&A market. This article takes a closer look at the role that private equity firms play in Germany and the strategies they employ.

2. A look back on M&A in 2024

KPMG’s recently published M&A Outlook 2025 examines the M&A strategies of corporates and private equity firms and the key factors that are expected to shape Germany’s M&A landscape in 2025. It also takes a look back at M&A activities in 2024.

Compared with 2023, a significant majority of the corporate executives surveyed reported increased activity on the deal market, with more than 60% claiming to have expanded their activities. The acquisition of technologies and capabilities proved a key driver for growth in M&A activity.

Disruptive technological change and ever-evolving business models are forcing businesses to transact in order to transform, with 80% of respondents citing the acquisition of technologies and capabilities as a crucial factor in future-proofing their business models.

High interest rates were seen as having the greatest influence on the willingness to buy and sell businesses, with two-thirds of those surveyed putting them among the top five market conditions shaping their decision-making. Although interest rates gradually began to decline in 2024 – and with them the cost of borrowing – it remains uncertain where they will head in the future. M&A activity is also influenced by mounting competitive pressure and geopolitical uncertainties, in particular cyber security threats, with a third of respondents citing the latter as one of the top five factors influencing their decisions. Among them, cyber security threats represent a particular source of anxiety, with 93% of geopolitical concerns attributable to cyber security risks.

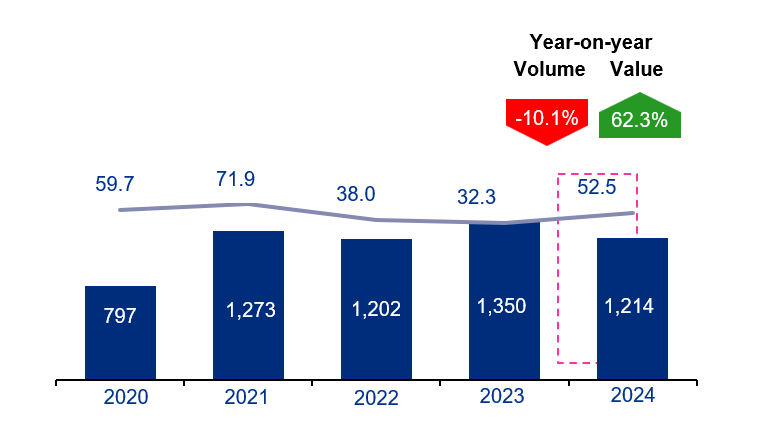

Fig. 1 PE-M&A-Deal-Aktivität nach Anzahl der Transaktionen und Deal Value (in Mrd. EUR)

Source: Research von KPMG in Deutschland, 2024 und 2025

Source: Research von KPMG in Deutschland, 2024 und 2025

2.1 Landmark PE M&A deals in 2024

The transaction count and with it deal activity on Germany’s PE M&A market fell short of expectations in 2024. The diagram below clearly shows the number of reported deals decline by 10.1% with a simultaneous 62.3% increase in deal value.

Overall, more than a thousand transactions are recorded in Germany each year. Below, the authors focus on the most significant registered PE M&A transactions with a private equity firm on the buy side.

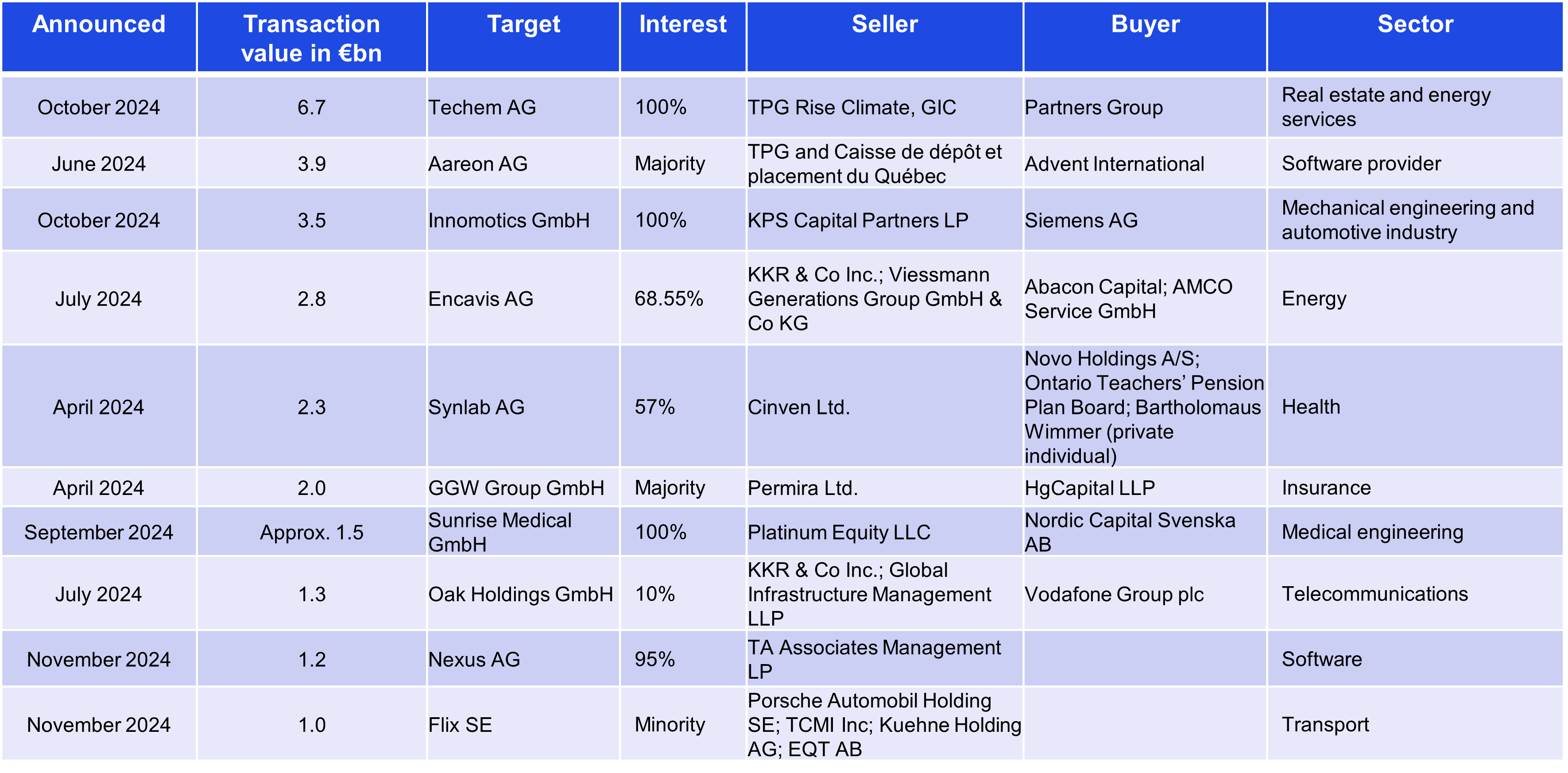

Fig. 2 Top 10 PE M&A transactions in 2024 by deal value (€bn)

Source: Research von KPMG in Deutschland, 2024 und 2025

Source: Research von KPMG in Deutschland, 2024 und 2025

Virtually all sectors saw major transactions in 2024, with software/tech, health and energy transition leading the way.

In early Q3 2024 it was announced that energy and metering service provider Techem AG had been acquired for a total of €6.7bn by TPG Texas Pacific Group (via its sustainable investment arm TPG Rise Climate) and Singapore sovereign wealth fund GIC. The vendors were Partners Group and its Canadian co-investors Caisse de dépôt et placement du Québec (CDPQ) and the Ontario Teacher’s Pension Plan. Techem is active in a non-cyclical market for energy efficiency solutions. It boasts high customer loyalty and a solid growth rate buoyed by a supportive regulatory framework, and helps decarbonise and digitalise the building sector – a core element of the energy transition and efforts to achieve net zero in Germany by 2045.

Aareon AG, which Advent sold to TPG and CDPQ at a deal value of €3.9bn, is a provider of SaaS solutions for Europe’s real estate industry. The company markets software solutions deployed in residential and commercial property management. TPG invested in Aareon via TPG Capital, its US and European private equity platform, acting in consortium with CDPQ, a global investment group that acquired a minority interest in Aareon together with TPG. Advent retains an interest in Aareon and has put up additional capital for a minority interest in the independent company.

US-based financial investor TA Associates secured a significant majority interest in software provider Nexus for €1.2bn. At the end of the acceptance period on 3 January 2025, the tender offer had been accepted by an impressive 94.95% of shares, including the 26.9% that key shareholders had offered for that purpose. TA Associates expects the deal to close during Q1 2025. Nexus specialises in developing software solutions for hospitals, psychiatric clinics, rehabilitation facilities and diagnostic centres.

Another key deal was KPS Capital Partners LP’s €3.5bn acquisition of Innomotics GmbH from Siemens AG. Innomotics GmbH, which specialises in the manufacture and sale of electric and industrial motors, exemplifies the continuing interest in industrial automation solutions and electric drive technologies. Investments in this area highlight the need to leverage automation and digitalisation to lock in long-term cost reductions, generate added value and remain competitive.

Another major transaction was the €2.8bn acquisition of Encavis AG by KKR & Co Inc. and Viessmann Generations Group GmbH & Co KG. Encavis AG is a leading operator of solar power plants and wind farms, underscoring the burgeoning interest in renewables in the context of the energy transition.

Strategic decisions led Cinven Ltd. to take Synlab AG private again following its IPO during the pandemic. Cinven Ltd. retains a 57% majority interest and the deal was valued at €2.3bn. In addition, Cinven has gained a strategic partner in Labcorp, which brings extensive industry expertise and holds a 15% minority interest. The deal is set to close in Q1 2025. This move makes it clear that investors are increasingly willing to make sizeable investments in the healthcare sector to capitalise on the growing demand for medical services.

In the medical engineering sector, Platinum Equity LLC acquired Sunrise Medical GmbH from Nordic Capital Svenska AB in a deal valued at some €1.5bn. Wheelchair manufacturer Sunrise Medical GmbH highlights the significance of medical engineering and medical aids in the healthcare sector. Nordic Capital took a two-pronged approach to this sale: It began by announcing an IPO for Sunrise Medical in May 2024, while at the same time – in a move now commonplace for major deals – negotiating a potential takeover with several investors.

Permira Ltd.’s €2.0bn acquisition of GGW Group GmbH from HgCapital LLP showcases the interest in insurance industry service providers. GGW Group GmbH, a provider of insurance services, offered an exit strategy for HgCapital LLP and shows the potential for growth and consolidation among insurance brokers.

These large transaction volumes clearly demonstrate that private equity firms are prepared to make substantial investments once suitable targets are available Major transactions stemmed from transformations at major corporates, investments in and partnerships with family-owned businesses, take-privates and a handful of successful fund-to-fund deals.

Another notable trend in 2024 was the increasing willingness of private equity firms to consider not just majority interests but minority shareholdings too. Examples include Cinven Ltd.’s acquisition of a minority interest in Fressnapf Tiernahrungs GmbH and the acquisition of a 10% stake in Oak Holdings GmbH by KKR & Co Inc. and Global Infrastructure Management LLP. Minority shareholdings enable investors to buy into promising businesses while retaining a certain amount of flexibility.

Overall, the PE M&A market was weaker than expected in 2024 and the sought-after recovery failed to materialise. The PE M&A market was influenced by high interest rates, competitive pressure and geopolitical uncertainties. Private equity firms focused on strategic acquisitions to strengthen and future-proof their business models.

3. Outlook for 2025

3.1 Forecast for the overall M&A market in 2025

The recovery on the M&A market forecast for 2024 is now expected to materialise in 2025. After a subdued year in 2024, corporates and private equity firms are now looking to the future with far more optimism and confidence.

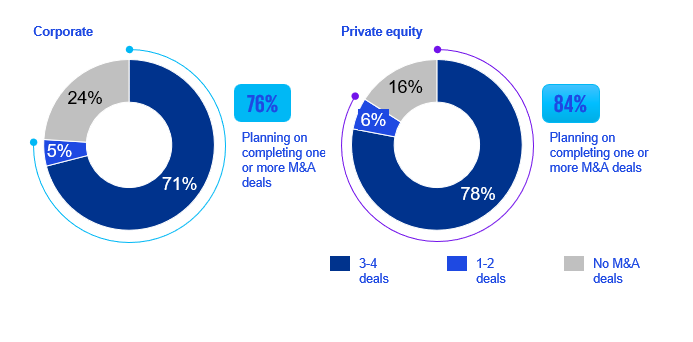

Fig. 3 M&A pipeline for 2025

Source: 2025 M&A outlook for German corporate and private equity dealmakers, KPMG in Deutschland 2024

Source: 2025 M&A outlook for German corporate and private equity dealmakers, KPMG in Deutschland 2024

A close look at the M&A Outlook 2025 reveals that the majority of German corporate and private equity decision-makers are predicting increased activity in the overall deal market. Private equity firms are more likely to be planning one or more deals, while corporates – though planning deals slightly less frequently – are more often aiming to pursue more than one deal in 2025.

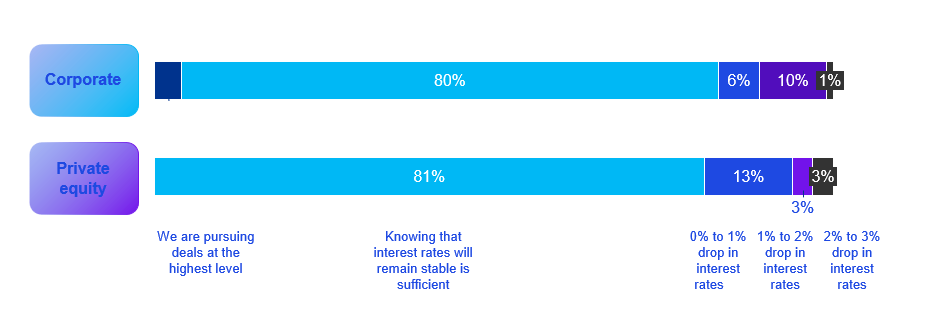

While deal activity is expected to increase, the market conditions that shape deal decisions – although better than in 2024 – remain challenging in some areas. The interest rate volatility of recent years has fuelled a desire for stability and predictability. The vast majority consider the current interest rate level to be acceptable and view stable interest rates in the near future as a positive development. A stable and predictable interest rate environment would help steady the market and potentially narrow the price expectation mismatch between buyers and sellers.

The following insights can be gleaned from the M&A Outlook 2025: High valuation expectations and market uncertainties will pose challenges but also create opportunities for strategic negotiations and value adjustments between sellers and buyers.

Despite these persistent uncertainties, many businesses have opted for a transact-to-transform approach, using M&A to reshape their business models and strengthen their long-term competitiveness. In this new business environment, and with cyber security risks increasing in severity, dealmakers should pursue thorough due diligence to mitigate risks and maximise value creation.

3.2 Strategic implications for private equity firms

Looking at the results of the M&A Outlook 2025, three key trends emerge for private equity firms in 2025:

Disciplined pricing: private equity firms have stepped up their pricing discipline to avoid overpaying and in anticipation that valuations will normalise further. This is particularly the case for funds with sufficient dry powder beyond 2025, since they are not forced to invest immediately and can pursue a wait-and-see strategy.

Enhanced due diligence: The limited availability of high-value assets investment opportunities requires razor-sharp enhanced due diligence that goes beyond what was traditionally the case and already includes detailed planning of future value creation levers. Careful due diligence locks in the long-term success of investments.

Enhanced deal origination and flexibility: Private equity firms have stepped up their deal origination efforts and have become way more flexible in terms of investments. There is a significant number of investments in strategic partnerships with family-owned businesses or large corporates who consider private equity firms as reliable

Fig. 4 The effect of interest rates

Source: 2025 M&A outlook for German corporate and private equity dealmakers, KPMG in Deutschland 2024

4. Conclusion

PE M&A activities in Germany in 2024 were dominated by a large number of small and medium-sized add-on acquisitions of portfolio companies, and in particular by a handful of major deals – primarily in software/tech, healthcare and energy transition. Despite global challenges such as geopolitical tensions and an uncertain interest rate environment, private equity firms continued to create lasting value through their investments and in doing so generate the returns required by their investors in the long term. A notable trend was the increasing use of minority interests to secure competitive advantages and ensure flexibility.

PE M&A activities are expected to grow significantly in 2025, with many private equity firms planning strategic deals to create lasting value and foster sustainable growth. Disciplined pricing, enhanced due diligence and sharpened deal origination efforts will play a pivotal role. Despite the ongoing uncertainties, corporates and private equity firms alike are committed to M&A as a means of transforming their business models and strengthening their long-term competitiveness.